11 hidden costs of buying a new home should be carefully considered by homebuyers. Beyond the down payment and mortgage, extra expenses, like inspections, taxes, insurance, and moving fees, can add up quickly.

According to The Wall Street Journal, homeowners spend approximately $1,180/month on hidden costs, including insurance, maintenance, and utilities. CNBC also reports that these expenses can reach $18,000 a year. For that reason, this article will help you understand hidden costs so you can budget smartly and avoid financial setbacks.

Key Takeaways:

- Budget for the 11 hidden costs of buying a home

- Research local fees to avoid costs that trap you in debt after a home purchase.

- Consult professionals for legal and closing cost guidance.

What Things You Should Know Before Buying a Home

Buying a home isn’t just about paying the mortgage and down payment. There are additional costs that many buyers don’t expect. Knowing them early will help you prepare your budget better.

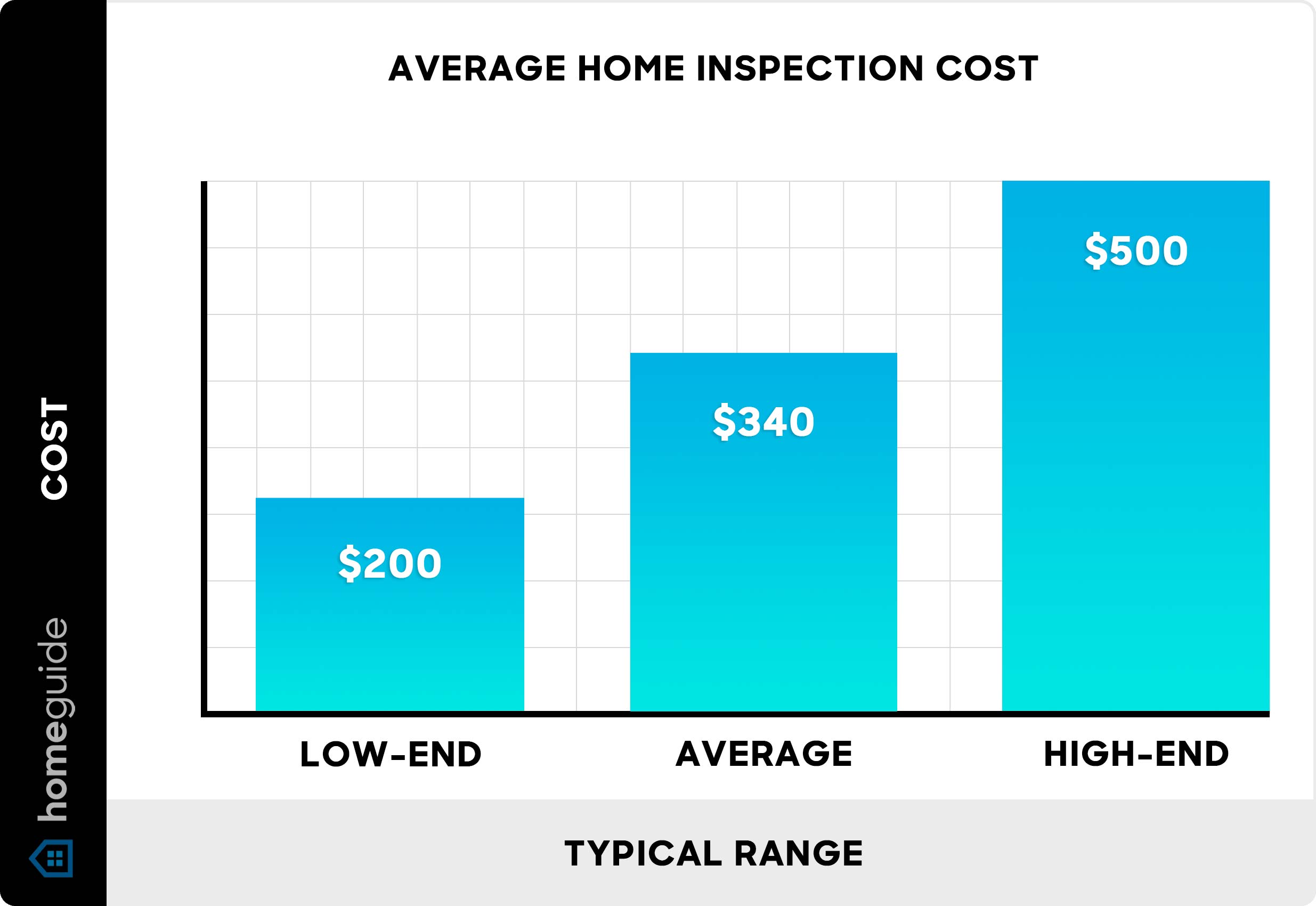

1. Home Inspection Fees

An inspector helps check the house for issues such as leaks, faulty wiring, or structural problems that may not be noticeable at first glance. The fee usually costs a few hundred dollars, but it’s worth it to help find problems early and save you from paying much more in repairs later.

2. Initial Repairs and Renovations

Among the 11 hidden costs of buying a home, repairs and renovations are important. These can include fixing structural issues, repairing plumbing and electrical systems, repainting, or replacing damaged floors. Renovations may also involve upgrading rooms, like bathrooms, or adding modern features to boost the property’s value.

Also Read: 7 Smart Financial Lessons That Explain How the Rich Stay Rich

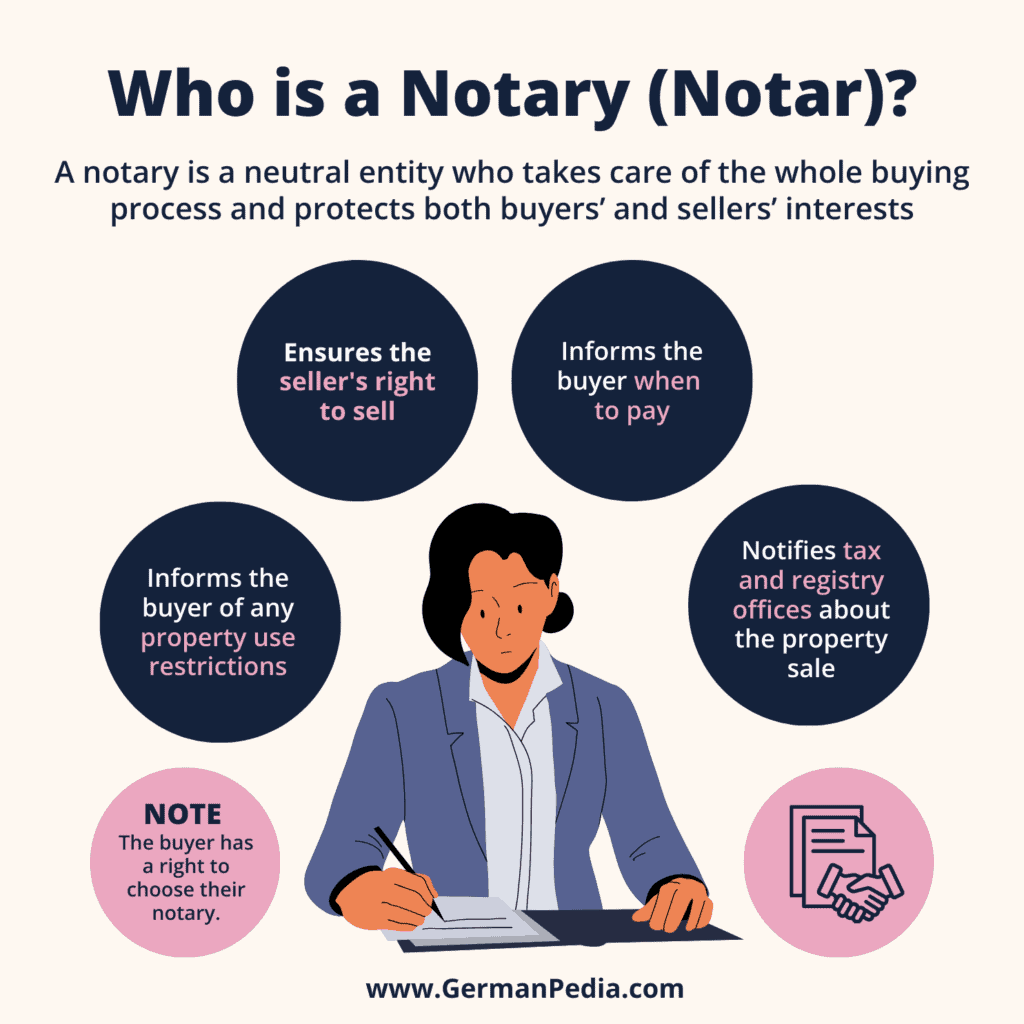

3. Notary and Legal Fees

Notary and Legal Fees cover the paperwork and legal steps needed to transfer property ownership. A notary or lawyer makes sure the contract is valid and all documents are handled correctly.

These fees can vary by state and the complexity of the sale, but setting money aside for them early helps avoid last-minute surprises. According to the American Bar Association, having a lawyer review real estate contracts can help protect buyers from common legal issues.

4. Homeowners Insurance

Your new house is protected by homeowners’ insurance against unforeseen circumstances like fire, theft, and natural disasters. The price varies according to your location, the value of the house, and the type of coverage you want.

While it’s an additional monthly or annual expense, having insurance provides peace of mind and financial protection if anything goes wrong.

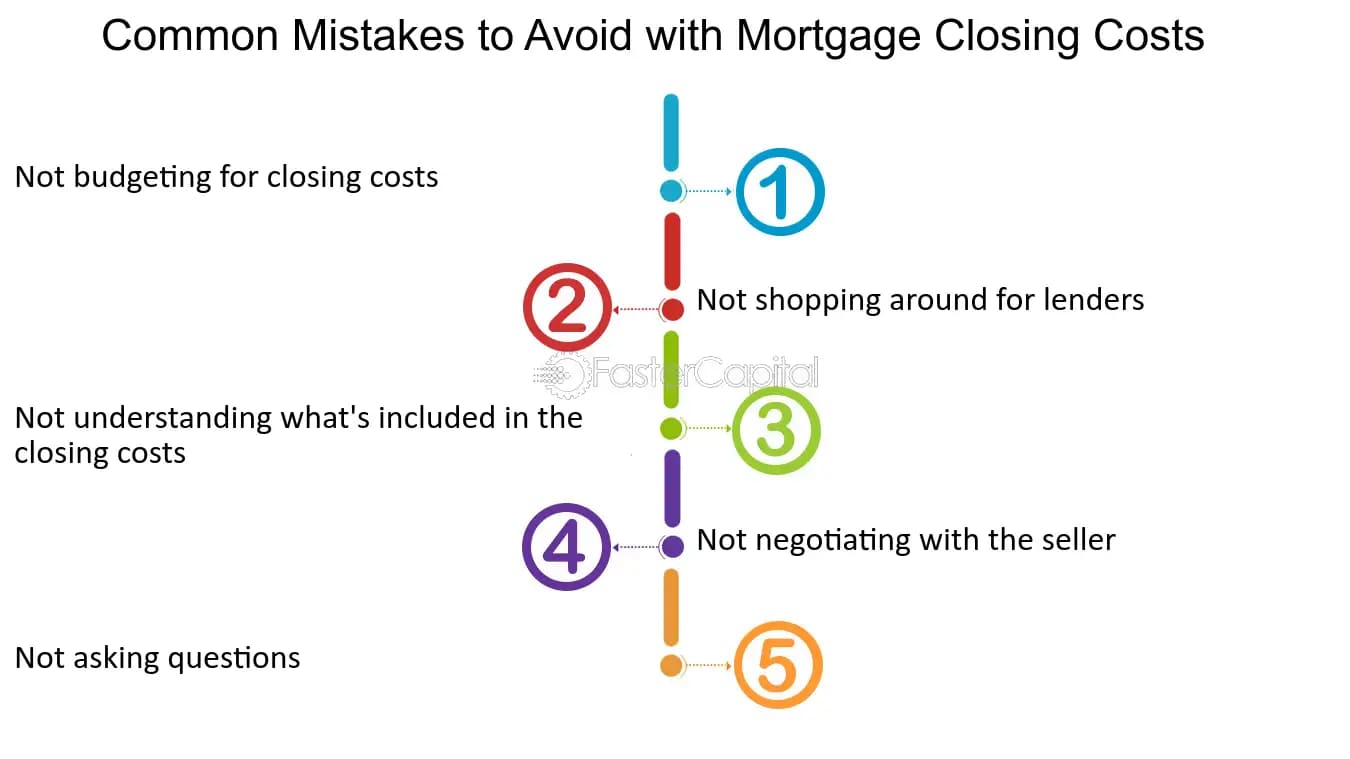

5. Mortgage Closing Costs

Mortgage Closing Costs are one of the 11 hidden costs of buying a home that can catch buyers off guard. These fees are paid when finalizing your home loan and can include loan origination, appraisals, title searches, and processing fees.

According to bankrate.com, costs typically range from 2% to 5% of the home’s purchase price. Knowing these costs in advance helps you plan your budget and avoid any surprises on closing day.

Also Read: Improve Your Lifestyle with 6 Best Habit Tracker App Choices

6. Ongoing Maintenance Costs

Ongoing Maintenance Costs are expenses that continue long after you move in. Regular upkeep like lawn care, pest control, cleaning, and minor repairs keeps your home in good condition and prevents bigger problems down the road.

Planning for these costs as part of your monthly budget ensures your home stays safe and comfortable without unexpected financial stress.

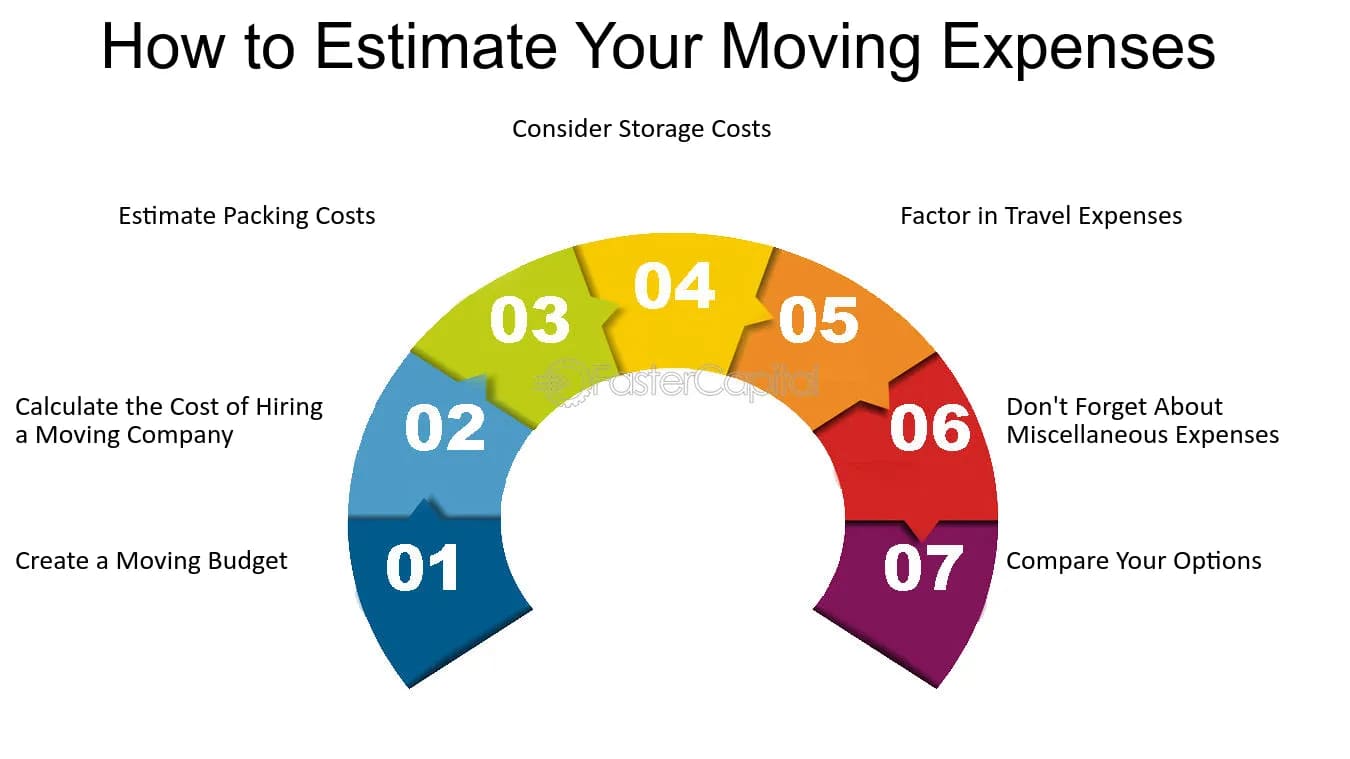

7. Moving Expenses

Moving Expenses can add up quickly, yet many buyers forget to plan for them. Moving companies, truck rentals, packing materials, and even short-term storage can all be expensive. By budgeting for these expenses in advance, you can make your move smoother and avoid last-minute financial stress.

8. Utility Setup and Deposits

Utility Setup and Deposits are often overlooked when budgeting for a new home. Starting services like electricity, water, gas, internet, and sometimes trash collection can require initial setup fees or security deposits. Planning for these costs ahead of time ensures you won’t face unexpected bills right after moving in.

Also Read: 15 Things to Sell to Make Money: Low-Cost Ideas With High-Profit

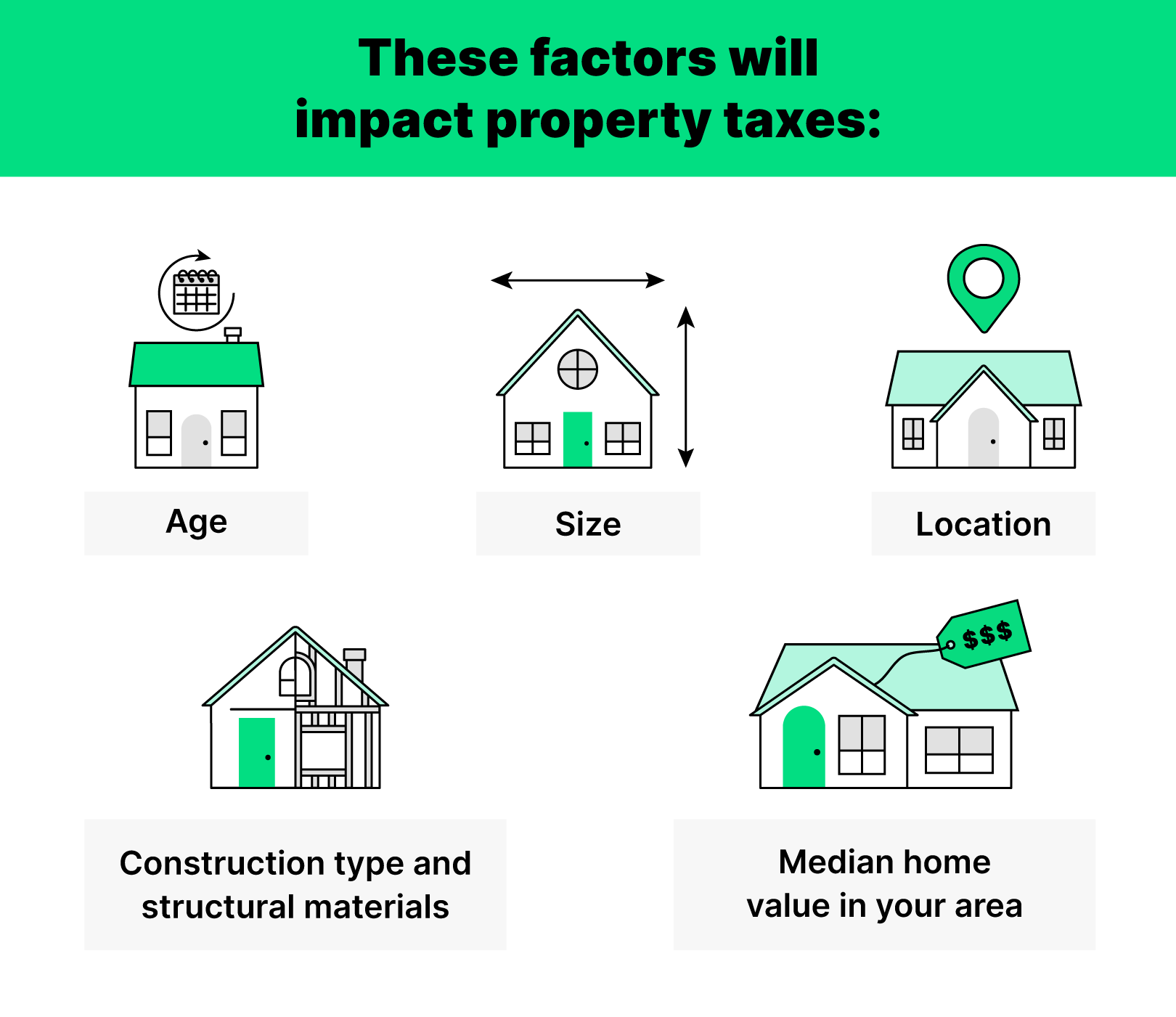

9. Property Taxes

Property Taxes can surprise many first-time buyers. Depending on the location and value of the home, they can add up to a significant yearly expense and are one of the costs that trap you in debt after home purchase if not planned for properly.

Sometimes these taxes are included in your mortgage payment, while other times you’ll need to pay them separately. Checking local rates before buying helps you avoid any unexpected financial strain.

10. Furniture and Appliances

Furniture and Appliances make your new house feel like home. Even if the home comes with some essentials, you may still need to buy items like beds, sofas, kitchen appliances, and storage solutions. Budgeting for these expenses in advance helps you settle in comfortably without surprises.

11. HOA Fees

HOA Fees are payments required if your home is part of a homeowners association, such as in a condo or planned community. These fees cover shared amenities, maintenance of common areas, and sometimes even security services.

While the amount varies depending on the community, including it in your budget ensures you’re not caught off guard by monthly or annual payments.

Also Read: The Best Way to Make Money on Savings for Beginners

Be Ready for Unexpected Expenses When Purchasing a Home

Understanding the 11 hidden costs of buying a home is key to avoiding financial stress after you move in. Expenses like inspections, insurance, taxes, and maintenance can add up fast. Therefore, you should plan ahead by saving an extra 5–10% of your home’s price, checking local fees, and reviewing contracts carefully.

Additionally, talking with a trusted real estate agent or financial advisor can also give you a clearer picture of what to expect. By knowing these costs, you’ll better understand how buying a home can impact financial independence and prepare yourself for long-term stability.